› Forums › General Discussions › Currency Strength

Tagged: currency strength

- This topic has 192 replies, 24 voices, and was last updated 1 year, 11 months ago by

simplex.

simplex.

- AuthorPosts

- March 14, 2015 at 5:07 am #5774

Hi All, this is similar to my explanation to one of our Brother PM, about my currency distance calculation (I don’t dare to called it strength..lol).. I post it here this kindergarten calculation, everybody who needed could read and I don’t need to repeat it when I received similar PM…lol.

At this weekend market break (for retail trader of course, since value keep moving 24/7).., my MT4 data give me;

EURUSD = 1.04952 USDJPY = 121.386 EURJPY = 127.389.

As we know the JPY ratio is 1:100 yen, so we should normalize it to become equal with other pairs ratio by divide it with 100.

EURUSD = 1.04952 (5 digits)

USDJPY = 121.386/100 = 1.21386 (5 digits)

EURJPY =127.389/100 = 1.27389 (5 digits)

from the above 3 pairs, we have 2 part USD value, 2 part EUR value, and 2 part JPY value.

when we add EURUSD with USDJPY we get = 1.04952 + 1.21386 = 2.26338 (this is values of 2 USD part 1 EUR part and 1 JPY part)

when we subtract EURUSDUSDJPY with EURJPY we get = 2.26338 – 1.27389 = 0.98949 (this is value of 2 USD part)

So, to get 1 part of USD we divide that value by 2 = 0.98949 / 2 = 0.494745

Next,

1 part of USD = 0.494745

1 part of EUR = EURUSD – 1 part of USD = 1.04952 – 0.494745 = 0.554775

1 part of JPY = USDJPY – 1 part of USD = 1.21386 – 0.494745 = 0.719115

Lets measure them from parity pole of 1 (in my own kindergarten opinion of course)

USD value = 1 – 0.494745 = 0.505255 or roughly 50.52 %

EUR value = 1 – 0.554775 = 0.445255 or roughly 44.52 %

JPY value = 1 – 0.719115 = 0.280885 or roughly 28.08 %

Well in my noob math, I think USD is 6% faster than EUR and 22.44% faster than JPY, and EUR is 16.44 % faster than JPY.

Hope you understand and have a nice week end

MTH

Intuition, Experiences and Common sense..

http://www.binaryoptionsedge.com/March 14, 2015 at 11:49 am #5775Actually before you do answer I will move this little bit forward as you have NO IDEA what are you talking about. You do not know how market structure works, not only FX, but overall. Faster we will go over it faster we reach the target. Don’t take it personally BlackStack, ok? Believe in whatever you want. 1.For paper money to exist there have to be something underlying as if there isn’t, you will have Zimbabwe in your country. So again what is it? 2. If we are in the world of Aristotle: in the whole there is more wealth in USE then in OWNERSHIP? What does it mean? Wealth in use and in ownership? 3. Bond market is THE PRIMARY MARKET as this is where it is all starts from macro side….or if you prefer from micro point of view “mr. Jones come to shop and BUY socks (to be easier this are not american socks as those were imported to US.) 4. 5 trillion a day market IS A FALLACY…think about it as most of you think about spot while FX contains futures, options and forwards…+ spot you trading/gambling at. Why is it fallacy? Tiny hint. Retail trader x trades 1 lot with retail trader y. One is selling and other is buying, both have 1000$ on their account….yet their trade in volume is larger than their accounts combined. How is that possible. That is FAKE side of the market – Tier 3- micro world of retail. Mercedes-Benz comes to DB and want to BUY 200 mln $ to fund their US operations…and pay in Euros…through the phone they say how much they want and at what price, DB will accept (as they are probably their dealer) and USE forward deliverable to close the deal. What this does to DB is this…..DB is now 200mil $ short (as they have Mercedes Euros) so any move in $ against them will create HOLE in their balance sheet (they will loose on the deal). In the other words DB HAS LONG EUR/USD position…..so they will hedge same amount on spot FX …….BUT TO DO IT SOMEBODY HAS TO TAKE OTHER SIDE OF THAT TRADE…. It will be either THEIR own client (on their internal exchange as every tier 1 bank their operate few) OR other banks if they send this quote to EBS/REUTERS…..and DB counter party lets say UBS ….and this bank have agreements as liquidity provider with brokers and other exchanges and they will show those “200mil” quote to them because they know if they hit that button UBS can hedge it instantly on EBS……so we have 200 mln in EBS, 200 mln to some brokers and 200 millions to some exchanges in total few times 200 mil liquidity (let say x5 = 1 bil) provided and in reality ONLY 200 millions liquidity. It is even worse than that as there are MANY MARKET participants and many quotes so market really multiplying liquidity levels…..if JPM and Citi are liquidity providers to currenex and they BOTH see 200 mln quote on EBS they will “show” 200 mln each to currenex clients that is 400mln in total. Why do you think that gave you LEVERAGE…CREDIT FOR FREE ??? Have you ever heard about credit for free?? They needed you as that risk taker, to spread it across market place and minimize the risk. 5 Trillion market is just fallacy for guys like you……HOT POTATO changing HANDS…..to simplify it….I have one mandarin in hand and you are allowed to hold it, every time bank/broker/speculator have touch it or holding it his bearing that risk and THEY WANT TO MOVE IT ON TO ANOTHER PARTY….and this party IS YOU…you bear the risk , you RETAIL TRADER you are risk taker…end user of the SPOT FX or any other speculator on ECN marketplace. And guys from above post tells me that primary drive of market is manipulation…..ok, I will

:) ps. I have to go with dogs , so I am sorry for any mistakes as written quickly. ps2. edited :D

:) ps. I have to go with dogs , so I am sorry for any mistakes as written quickly. ps2. edited :DActually before you do answer I will move this little bit forward as you have NO IDEA what are you talking about. You do not know how market structure works, not only FX, but overall. Faster we will go over it faster we reach the target. Don’t take it personally BlackStack, ok? Believe in whatever you want. 1.For paper money to exist there have to be something underlying as if there isn’t, you will have Zimbabwe in your country. So again what is it? 2. If we are in the world of Aristotle: in the whole there is more wealth in USE then in OWNERSHIP? What does it mean? Wealth in use and in ownership? 3. Bond market is THE PRIMARY MARKET as this is where it is all starts from macro side….or if you prefer from micro point of view “mr. Jones come to shop and BUY socks (to be easier this are not american socks as those were imported to US.) 4. 5 trillion a day market IS A FALLACY…think about it as most of you think about spot while FX contains futures, options and forwards…+ spot you trading/gambling at. Why is it fallacy? Tiny hint. Retail trader x trades 1 lot with retail trader y. One is selling and other is buying, both have 1000$ on their account….yet their trade in volume is larger than their accounts combined. How is that possible. That is FAKE side of the market – Tier 3- micro world of retail. Mercedes-Benz comes to DB and want to BUY 200 mln $ to fund their US operations…and pay in Euros…through the phone they say how much they want and at what price, DB will accept (as they are probably their dealer) and USE forward deliverable to close the deal. What this does to DB is this…..DB is now 200mil $ short (as they have Mercedes Euros) so any move in $ against them will create HOLE in their balance sheet (they will loose on the deal). In the other words DB HAS LONG EUR/USD position…..so they will hedge same amount on spot FX …….BUT TO DO IT SOMEBODY HAS TO TAKE OTHER SIDE OF THAT TRADE…. It will be either THEIR own client (on their internal exchange as every tier 1 bank their operate few) OR other banks if they send this quote to EBS/REUTERS…..and DB counter party lets say UBS ….and this bank have agreements as liquidity provider with brokers and other exchanges and they will show those “200mil” quote to them because they know if they hit that button UBS can hedge it instantly on EBS……so we have 200 mln in EBS, 200 mln to some brokers and 200 millions to some exchanges in total few times 200 mil liquidity (let say x5 = 1 bil) provided and in reality ONLY 200 millions liquidity. It is even worse than that as there are MANY MARKET participants and many quotes so market really multiplying liquidity levels…..if JPM and Citi are liquidity providers to currenex and they BOTH see 200 mln quote on EBS they will “show” 200 mln each to currenex clients that is 400mln in total. Why do you think that gave you LEVERAGE…CREDIT FOR FREE ??? Have you ever heard about credit for free?? They needed you as that risk taker, to spread it across market place and minimize the risk. 5 Trillion market is just fallacy for guys like you……HOT POTATO changing HANDS…..to simplify it….I have one mandarin in hand and you are allowed to hold it, every time bank/broker/speculator have touch it or holding it his bearing that risk and THEY WANT TO MOVE IT ON TO ANOTHER PARTY….and this party IS YOU…you bear the risk , you RETAIL TRADER you are risk taker…end user of the SPOT FX or any other speculator on ECN marketplace. And guys from above post tells me that primary drive of market is manipulation…..ok, I will

:) ps. I have to go with dogs , so I am sorry for any mistakes as written quickly. ps2. edited :Dgood revolution tell them this how the dealer will do hedge that’s all excellent post you really know this stuff well revolution this how the broker does

March 14, 2015 at 4:37 pm #5779Umm.. don’t you think that ‘intrinsic value’ term is also result from an agreement between societies (not all human, only who that called them self ‘civilized societies’).. because when I try to trade with remote island tribe to exchange my gold nugget with banana, they throw out my gold nugget…lol… (sorry it’s only a joke..). Best Regards MTH

Hi Kiads,

I think you are talking about a barter trade instead of a monetary system. That remote tribe must also know that a banana is a poor form of money, since if they store a room fill of them in time they would be worthless. When something is chosen as money its value is relative to other things, which is best determined by the market. An ounce of gold is always worth an ounce of gold.

What you are exchanging with money is really stored human labour. When central banks are printing trillions of new dollars, euros, etc. into existence they are making human labour worthless. To get a new ounce of gold into a monetary system takes a lot of human effort. The banks are making new currency notes with minimal effort, more so with digital currency. The current corrupt fiat money system must end.

March 14, 2015 at 7:06 pm #5780Umm.. don’t you think that ‘intrinsic value’ term is also result from an agreement between societies (not all human, only who that called them self ‘civilized societies’).. because when I try to trade with remote island tribe to exchange my gold nugget with banana, they throw out my gold nugget…lol… (sorry it’s only a joke..). Best Regards MTH

Hi Kiads, I think you are talking about a barter trade instead of a monetary system. That remote tribe must also know that a banana is a poor form of money, since if they store a room fill of them in time they would be worthless. When something is chosen as money its value is relative to other things, which is best determined by the market. An ounce of gold is always worth an ounce of gold. What you are exchanging with money is really stored human labour. When central banks are printing trillions of new dollars, euros, etc. into existence they are making human labour worthless. To get a new ounce of gold into a monetary system takes a lot of human effort. The banks are making new currency notes with minimal effort, more so with digital currency. The current corrupt fiat money system must end.

Ah.. Yes, forgive me Brother, since I only understand about ‘trade’, almost everyday I barter my US Dollar with Euro or other barter tools.. lol, last time I remember that 1 Euro worth 1.04946 US dollar I dunno about next Monday.. , and I still can’t understand the different between exchange and barter.. if any..

Best Regards

MTH

Intuition, Experiences and Common sense..

http://www.binaryoptionsedge.com/March 14, 2015 at 7:29 pm #5781Well actually Kiads you raise a good point about exchange of fiat currencies and barter. Barter is exchange of goods or services directly without the use of money. Since currencies are not money, maybe then it is like barter.

Anyway hopefully this current system will send soon (maybe by October) and a sound money system will be used again. Enjoy your FX trading while you can.

March 16, 2015 at 7:21 am #57834. 5 trillion a day market IS A FALLACY…think about it as most of you think about spot while FX contains futures, options and forwards…+ spot you trading/gambling at. Why is it fallacy? Tiny hint. Retail trader x trades 1 lot with retail trader y. One is selling and other is buying, both have 1000$ on their account….yet their trade in volume is larger than their accounts combined. How is that possible. That is FAKE side of the market – Tier 3- micro world of retail. Mercedes-Benz comes to DB and want to BUY 200 mln $ to fund their US operations…and pay in Euros…through the phone they say how much they want and at what price, DB will accept (as they are probably their dealer) and USE forward deliverable to close the deal. What this does to DB is this…..DB is now 200mil $ short (as they have Mercedes Euros) so any move in $ against them will create HOLE in their balance sheet (they will loose on the deal). In the other words DB HAS LONG EUR/USD position…..so they will hedge same amount on spot FX …….BUT TO DO IT SOMEBODY HAS TO TAKE OTHER SIDE OF THAT TRADE…. It will be either THEIR own client (on their internal exchange as every tier 1 bank their operate few) OR other banks if they send this quote to EBS/REUTERS…..and DB counter party lets say UBS ….and this bank have agreements as liquidity provider with brokers and other exchanges and they will show those “200mil” quote to them because they know if they hit that button UBS can hedge it instantly on EBS……so we have 200 mln in EBS, 200 mln to some brokers and 200 millions to some exchanges in total few times 200 mil liquidity (let say x5 = 1 bil) provided and in reality ONLY 200 millions liquidity. It is even worse than that as there are MANY MARKET participants and many quotes so market really multiplying liquidity levels…..

Hi Revolution,

I was reading this thread and your style seemed familiar to me. Then I read the above example which is exactly the same as orderflowtrading.com’s Lesson 3 (http://www.orderflowtrading.com/LearnOrderFlow/Mindset/Lesson3.aspx).

Is that correct? I mean are you orderflowtrading.com ?

Best regards…

Nothing has ever motivated me more than this...

March 16, 2015 at 11:15 am #57864. 5 trillion a day market IS A FALLACY…think about it as most of you think about spot while FX contains futures, options and forwards…+ spot you trading/gambling at. Why is it fallacy? Tiny hint. Retail trader x trades 1 lot with retail trader y. One is selling and other is buying, both have 1000$ on their account….yet their trade in volume is larger than their accounts combined. How is that possible. That is FAKE side of the market – Tier 3- micro world of retail. Mercedes-Benz comes to DB and want to BUY 200 mln $ to fund their US operations…and pay in Euros…through the phone they say how much they want and at what price, DB will accept (as they are probably their dealer) and USE forward deliverable to close the deal. What this does to DB is this…..DB is now 200mil $ short (as they have Mercedes Euros) so any move in $ against them will create HOLE in their balance sheet (they will loose on the deal). In the other words DB HAS LONG EUR/USD position…..so they will hedge same amount on spot FX …….BUT TO DO IT SOMEBODY HAS TO TAKE OTHER SIDE OF THAT TRADE…. It will be either THEIR own client (on their internal exchange as every tier 1 bank their operate few) OR other banks if they send this quote to EBS/REUTERS…..and DB counter party lets say UBS ….and this bank have agreements as liquidity provider with brokers and other exchanges and they will show those “200mil” quote to them because they know if they hit that button UBS can hedge it instantly on EBS……so we have 200 mln in EBS, 200 mln to some brokers and 200 millions to some exchanges in total few times 200 mil liquidity (let say x5 = 1 bil) provided and in reality ONLY 200 millions liquidity. It is even worse than that as there are MANY MARKET participants and many quotes so market really multiplying liquidity levels…..

Hi Revolution, I was reading this thread and your style seemed familiar to me. Then I read the above example which is exactly the same as orderflowtrading.com’s Lesson 3 (http://www.orderflowtrading.com/LearnOrderFlow/Mindset/Lesson3.aspx). Is that correct? I mean are you orderflowtrading.com ? Best regards…

No, I am not. Darkstar is the originator of the website I believe….similarity accidental, maybe because I have read it long time ago and it stayed in my head…anyways still works the same…

March 20, 2015 at 5:52 pm #5866PS. btw I’m waiting my next ‘soon’ in W1 point of view..for EURUSD..

Ta Daaa… that ‘soon’ is this week…lol…

Have a nice week end for all….

Best Regards

MTH

Intuition, Experiences and Common sense..

http://www.binaryoptionsedge.com/March 24, 2015 at 2:16 am #5921PS. btw I’m waiting my next ‘soon’ in W1 point of view..for EURUSD..

Ta Daaa… that ‘soon’ is this week…lol… Have a nice week end for all…. Best Regards MTH

I hope you not thinking about “that soon”…:D ? When you dive you have to take up some air sometimes. I would follow OIL this time…:)

March 29, 2015 at 9:10 am #6048Great content in this forum.

Love this thread, I also use a spaghetti indicators based on moving averages, sometimes it works and sometimes not, any development of this point has my attention

In every post I’ve read so far there is something that I have thought about and something that I had NOT thought instead, thank you all for sharing your knowledge.March 30, 2015 at 8:19 am #6059Hi All, this is similar to my explanation to one of our Brother PM, about my currency distance calculation (I don’t dare to called it strength..lol).. I post it here this kindergarten calculation, everybody who needed could read and I don’t need to repeat it when I received similar PM…lol. At this weekend market break (for retail trader of course, since value keep moving 24/7).., my MT4 data give me; EURUSD = 1.04952 USDJPY = 121.386 EURJPY = 127.389. As we know the JPY ratio is 1:100 yen, so we should normalize it to become equal with other pairs ratio by divide it with 100. EURUSD = 1.04952 (5 digits) USDJPY = 121.386/100 = 1.21386 (5 digits) EURJPY =127.389/100 = 1.27389 (5 digits) from the above 3 pairs, we have 2 part USD value, 2 part EUR value, and 2 part JPY value. when we add EURUSD with USDJPY we get = 1.04952 + 1.21386 = 2.26338 (this is values of 2 USD part 1 EUR part and 1 JPY part) when we subtract EURUSDUSDJPY with EURJPY we get = 2.26338 – 1.27389 = 0.98949 (this is value of 2 USD part) So, to get 1 part of USD we divide that value by 2 = 0.98949 / 2 = 0.494745 Next, 1 part of USD = 0.494745 1 part of EUR = EURUSD – 1 part of USD = 1.04952 – 0.494745 = 0.554775 1 part of JPY = USDJPY – 1 part of USD = 1.21386 – 0.494745 = 0.719115 Lets measure them from parity pole of 1 (in my own kindergarten opinion of course) USD value = 1 – 0.494745 = 0.505255 or roughly 50.52 % EUR value = 1 – 0.554775 = 0.445255 or roughly 44.52 % JPY value = 1 – 0.719115 = 0.280885 or roughly 28.08 % Well in my noob math, I think USD is 6% faster than EUR and 22.44% faster than JPY, and EUR is 16.44 % faster than JPY. Hope you understand and have a nice week end MTH

Dear Kiads,

Right now I’m trying to make an analogy between Impulse-Momentum concept of physics and Price Action of FX market. I have some “Similarity Variables” available for “Mass” and “Velocity”. Hard part is to find similarity variables for “Density” and “Force”. I think Density is inversely correlated with Volatility and Force is what you guys talk about -and I guess successfully use- Currency Strength.

I’ll open a thread solely on that once I get a reliable analogy.

And your description above will be useful for the anticipation of the next -target- price.

Thanks…

Best regards.

Nothing has ever motivated me more than this...

March 30, 2015 at 10:56 am #6060Right now I’m trying to make an analogy between Impulse-Momentum concept of physics and Price Action of FX market. I have some “Similarity Variables” available for “Mass” and “Velocity”. Hard part is to find similarity variables for “Density” and “Force”. I think Density is inversely correlated with Volatility and Force is what you guys talk about -and I guess successfully use- Currency Strength.

Analogies between physics and trading are coming to my mind frequently, and whenever it happens I’m trying to step back a little and ask myself ‘Is that really appropriate?’ Anyway, I’d be interested in discussing that topic further.

Talking about density: if you’re having Newton’s laws of mechanics in mind as an analogy, then you’d need density only if you’re having physical volume (not trading volume) as a given variable, IMO. Then what’s the analogy of physical volume in trading?

I think the main problem here would be that according to Newtonian Mechanics all masses are acting very ‘well-behaved’. Having a constant acceleration of 9.81 m/ss and neglecting friction makes it easy to calculate when the apple hits Newton’s hat. But are FX markets really that well-behaved? I’m afraid you’d need more sophisticated models to describe FX prices using physical analogies.

Anyway, adding physical volume would be a first step to implement nonlinear effects of friction in the formula.

A good trader is a realist who wants to grab a chunk from the body of a trend, leaving top- and bottom-fishing to people on an ego trip. (Dr. Alexander Elder)

March 30, 2015 at 11:28 am #6065Hi All, this is similar to my explanation to one of our Brother PM, about my currency distance calculation (I don’t dare to called it strength..lol).. I post it here this kindergarten calculation, everybody who needed could read and I don’t need to repeat it when I received similar PM…lol. At this weekend market break (for retail trader of course, since value keep moving 24/7).., my MT4 data give me; EURUSD = 1.04952 USDJPY = 121.386 EURJPY = 127.389. As we know the JPY ratio is 1:100 yen, so we should normalize it to become equal with other pairs ratio by divide it with 100. EURUSD = 1.04952 (5 digits) USDJPY = 121.386/100 = 1.21386 (5 digits) EURJPY =127.389/100 = 1.27389 (5 digits) from the above 3 pairs, we have 2 part USD value, 2 part EUR value, and 2 part JPY value. when we add EURUSD with USDJPY we get = 1.04952 + 1.21386 = 2.26338 (this is values of 2 USD part 1 EUR part and 1 JPY part) when we subtract EURUSDUSDJPY with EURJPY we get = 2.26338 – 1.27389 = 0.98949 (this is value of 2 USD part) So, to get 1 part of USD we divide that value by 2 = 0.98949 / 2 = 0.494745 Next, 1 part of USD = 0.494745 1 part of EUR = EURUSD – 1 part of USD = 1.04952 – 0.494745 = 0.554775 1 part of JPY = USDJPY – 1 part of USD = 1.21386 – 0.494745 = 0.719115 Lets measure them from parity pole of 1 (in my own kindergarten opinion of course) USD value = 1 – 0.494745 = 0.505255 or roughly 50.52 % EUR value = 1 – 0.554775 = 0.445255 or roughly 44.52 % JPY value = 1 – 0.719115 = 0.280885 or roughly 28.08 % Well in my noob math, I think USD is 6% faster than EUR and 22.44% faster than JPY, and EUR is 16.44 % faster than JPY. Hope you understand and have a nice week end MTH

Dear Kiads, Right now I’m trying to make an analogy between Impulse-Momentum concept of physics and Price Action of FX market. I have some “Similarity Variables” available for “Mass” and “Velocity”. Hard part is to find similarity variables for “Density” and “Force”. I think Density is inversely correlated with Volatility and Force is what you guys talk about -and I guess successfully use- Currency Strength. I’ll open a thread solely on that once I get a reliable analogy. And your description above will be useful for the anticipation of the next -target- price.

Thanks… Best regards.Hi Brother, from my noob understanding about physics , maybe we could say Density as ‘World Market Influence Share’ ratio between major currencies..

We’re not measuring single object, but multiple objects (at least major currencies), that interact each others and create chain reaction..

just like combat aircraft radar facing multiple enemy aircraft. So, let’s think about missile target locking system, how their computer algos could ‘react’ and ‘corrected’ any next evading attempt movement of enemy aircraft that already ‘locked’. Remember that the algo program must be more highly sophisticated rather than needed for ‘locking’ pair movements, since the enemy aircraft could move anywhere in 3 dimension surface, while price could only move in 2 diagonal ways.. forward lol.

Wish You All The Best

MTH

Intuition, Experiences and Common sense..

http://www.binaryoptionsedge.com/March 30, 2015 at 11:41 am #6066… Remember that the algo program must be more highly sophisticated rather than needed for ‘locking’ pair movements, since the enemy aircraft could move anywhere in 3 dimension surface, while price could only move in 2 diagonal ways.. [/quote]

You mean 45 and 315 degrees..?Nothing has ever motivated me more than this...

March 30, 2015 at 1:41 pm #6067… Remember that the algo program must be more highly sophisticated rather than needed for ‘locking’ pair movements, since the enemy aircraft could move anywhere in 3 dimension surface, while price could only move in 2 diagonal ways..

You mean 45 and 315 degrees..?[/quote]

Ideally Yes Brother, just diagonally up or diagonally down to the right side of our chart..lol, and 100% sure they never comeback to the left side…hehehe…

MTH

Intuition, Experiences and Common sense..

http://www.binaryoptionsedge.com/April 7, 2015 at 9:09 pm #6177Hey, brother Kiads, how has your currency strength experiment been working over the last month? I thought it was exciting to see your progress, even if I’m just spectating. ;) (And if you’d prefer not to speak about it, I won’t mind.)

PS. I failed to defending my 7 loss positions…thanks to NFP …lol Don’t bother to look at the profit value is not USD, is only IDR.. hehehe..

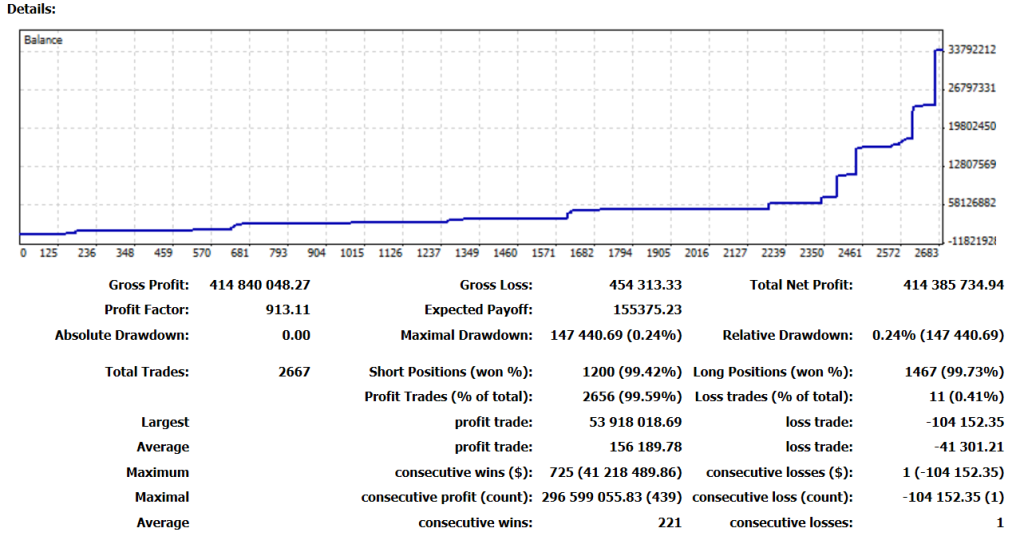

April 29, 2015 at 8:20 pm #6448

April 29, 2015 at 8:20 pm #6448… So Kiads here is giving you best advice you can get…experience in the end will make you profitable but you have to watch that staff, feel it.

Dear Kiads,

I believe you can predict the next movement. Please see the attachment.

Attachments:

You must be logged in to view attached files.Nothing has ever motivated me more than this...

May 7, 2015 at 5:53 am #6541Hi G,

1) The “Gadi Currencies” is the same as Spaghetti in this thread ?

2) How to calculate the cross Strength if we just know the major pairs ?

Example: If we know the Close price of EURUSD & USDJPY only (these are the major pairs). How can we get the strength of each currency, is it possible ? We have 3 variables (EUR, USD, JPY), but we only have 2 equations (2 pairs). Kiads use the cross pair EURJPY as addition (in order to get 3 equations).Thanks in advance.

May 7, 2015 at 1:10 pm #6544Hi G, 1) The “Gadi Currencies” is the same as Spaghetti in this thread ? 2) How to calculate the cross Strength if we just know the major pairs ? Example: If we know the Close price of EURUSD & USDJPY only (these are the major pairs). How can we get the strength of each currency, is it possible ? We have 3 variables (EUR, USD, JPY), but we only have 2 equations (2 pairs). Kiads use the cross pair EURJPY as addition (in order to get 3 equations). Thanks in advance.

The “ForexGT Spaghetti” is an improvement on the “Gadi Currencies” (currently not shared). You can use it – it’s good enough and you got many screenshots on how to use.

EURUSD * USDJPY = EURJPY, so why do you need it? …and the same goes to ALL other crosses.

Minor deviation in EURJPY price from the above formula (due to delays or mis-pricing) are immediatly corrected within miliseconds or seconds – and they will introduce errors, noise and inaccuracy to Currency-Strength indicators, if used.

If you use crosses in Currency-Strength indicator – you are adding 21 potential small errors and “noises” to that indie.

G.

May 7, 2015 at 1:19 pm #6545Hi G, 1) The “Gadi Currencies” is the same as Spaghetti in this thread ? 2) How to calculate the cross Strength if we just know the major pairs ? Example: If we know the Close price of EURUSD & USDJPY only (these are the major pairs). How can we get the strength of each currency, is it possible ? We have 3 variables (EUR, USD, JPY), but we only have 2 equations (2 pairs). Kiads use the cross pair EURJPY as addition (in order to get 3 equations). Thanks in advance.

The “ForexGT Spaghetti” is an improvement on the “Gadi Currencies” (currently not shared). You can use it – it’s good enough and you got many screenshots on how to use. EURUSD * USDJPY = EURJPY, so why do you need it? G.

OMG, you are right about EURJPY …. and thanks a lot for “Gadi Currencies” and others …

Edit : Could you please give me a clue on how to get value of each Currency (total 8 currencies) from that 7 major pairs (without cross pair) ?

Thanks in advance-

This reply was modified 11 years, 2 months ago by smallcat.

May 7, 2015 at 1:27 pm #6546Hi G, 1) The “Gadi Currencies” is the same as Spaghetti in this thread ? 2) How to calculate the cross Strength if we just know the major pairs ? Example: If we know the Close price of EURUSD & USDJPY only (these are the major pairs). How can we get the strength of each currency, is it possible ? We have 3 variables (EUR, USD, JPY), but we only have 2 equations (2 pairs). Kiads use the cross pair EURJPY as addition (in order to get 3 equations). Thanks in advance.

The “ForexGT Spaghetti” is an improvement on the “Gadi Currencies” (currently not shared). You can use it – it’s good enough and you got many screenshots on how to use. EURUSD * USDJPY = EURJPY, so why do you need it? G.

OMG, you are right about EURJPY …. and thanks a lot for “Gadi Currencies” and others …

OMG = Oh, My Gadi… ;-}

G.

May 7, 2015 at 1:40 pm #6548Hi G, 1) The “Gadi Currencies” is the same as Spaghetti in this thread ? 2) How to calculate the cross Strength if we just know the major pairs ? Example: If we know the Close price of EURUSD & USDJPY only (these are the major pairs). How can we get the strength of each currency, is it possible ? We have 3 variables (EUR, USD, JPY), but we only have 2 equations (2 pairs). Kiads use the cross pair EURJPY as addition (in order to get 3 equations). Thanks in advance.

The “ForexGT Spaghetti” is an improvement on the “Gadi Currencies” (currently not shared). You can use it – it’s good enough and you got many screenshots on how to use. EURUSD * USDJPY = EURJPY, so why do you need it? G.

OMG, you are right about EURJPY …. and thanks a lot for “Gadi Currencies” and others …

Edit : Could you please give me a clue on how to get value of each Currency (total 8 currencies) from that 7 major pairs (without cross pair) ? Thanks in advanceTake a look at the example of EURJPY (cross):

it is built with EURUSD and USDJPY.

If you buy EURUSD and buy USDJPY – you basically SELL the USD in EURUSD and BUY the USD in USDJPY. Since you sell and buy the USD at the same time, it is eliminated – and you are left with EURJPY (EUR bought and JPY sold).

The same goes to EURGBP which is built by EURUSD & GBPUSD. Since the USD is on the same side in those cases we just DIVIDE the EURUSD/GBPUSD = EURGBP.

Same goes to each and every one of the other 21 crosses.

G.

May 7, 2015 at 2:02 pm #6549Hi G, 1) The “Gadi Currencies” is the same as Spaghetti in this thread ? 2) How to calculate the cross Strength if we just know the major pairs ? Example: If we know the Close price of EURUSD & USDJPY only (these are the major pairs). How can we get the strength of each currency, is it possible ? We have 3 variables (EUR, USD, JPY), but we only have 2 equations (2 pairs). Kiads use the cross pair EURJPY as addition (in order to get 3 equations). Thanks in advance.

The “ForexGT Spaghetti” is an improvement on the “Gadi Currencies” (currently not shared). You can use it – it’s good enough and you got many screenshots on how to use. EURUSD * USDJPY = EURJPY, so why do you need it? G.

OMG, you are right about EURJPY …. and thanks a lot for “Gadi Currencies” and others …

Edit : Could you please give me a clue on how to get value of each Currency (total 8 currencies) from that 7 major pairs (without cross pair) ? Thanks in advanceTake a look at the example of EURJPY (cross): it is built with EURUSD and USDJPY. If you buy EURUSD and buy USDJPY – you basically SELL the USD in EURUSD and BUY the USD in USDJPY. Since you sell and buy the USD at the same time, it is eliminated – and you are left with EURJPY (EUR bought and JPY sold). The same goes to EURGBP which is built by EURUSD & GBPUSD. Since the USD is on the same side in those cases we just DIVIDE the EURUSD/GBPUSD = EURGBP. Same goes to each and every one of the other 21 crosses. G.

Thanks G. And how can i get the USD or EUR currency only , so i can do : USD = z * USD ?

May 7, 2015 at 4:36 pm #6553Hi G, 1) The “Gadi Currencies” is the same as Spaghetti in this thread ? 2) How to calculate the cross Strength if we just know the major pairs ? Example: If we know the Close price of EURUSD & USDJPY only (these are the major pairs). How can we get the strength of each currency, is it possible ? We have 3 variables (EUR, USD, JPY), but we only have 2 equations (2 pairs). Kiads use the cross pair EURJPY as addition (in order to get 3 equations). Thanks in advance.

The “ForexGT Spaghetti” is an improvement on the “Gadi Currencies” (currently not shared). You can use it – it’s good enough and you got many screenshots on how to use. EURUSD * USDJPY = EURJPY, so why do you need it? G.

OMG, you are right about EURJPY …. and thanks a lot for “Gadi Currencies” and others …

Edit : Could you please give me a clue on how to get value of each Currency (total 8 currencies) from that 7 major pairs (without cross pair) ? Thanks in advanceTake a look at the example of EURJPY (cross): it is built with EURUSD and USDJPY. If you buy EURUSD and buy USDJPY – you basically SELL the USD in EURUSD and BUY the USD in USDJPY. Since you sell and buy the USD at the same time, it is eliminated – and you are left with EURJPY (EUR bought and JPY sold). The same goes to EURGBP which is built by EURUSD & GBPUSD. Since the USD is on the same side in those cases we just DIVIDE the EURUSD/GBPUSD = EURGBP. Same goes to each and every one of the other 21 crosses. G.

Thanks G. And how can i get the USD or EUR currency only , so i can do : USD = z * USD ?

You need to find the diff movement of each currency pair. (d) is the diff between current and previous price, or other factor.

You shouls decide what are the optimized definitions of “current” and “previous” price.

USD = (EURUSDd + GBPUSDd + AUDUSDd + NZDUSDd + USDCHFd + USDJPYd + USDCADd) /7

The above result can be multilied by the currency market share, or other factor(s).

G.

May 8, 2015 at 5:27 pm #6573Hi G, 1) The “Gadi Currencies” is the same as Spaghetti in this thread ? 2) How to calculate the cross Strength if we just know the major pairs ? Example: If we know the Close price of EURUSD & USDJPY only (these are the major pairs). How can we get the strength of each currency, is it possible ? We have 3 variables (EUR, USD, JPY), but we only have 2 equations (2 pairs). Kiads use the cross pair EURJPY as addition (in order to get 3 equations). Thanks in advance.

The “ForexGT Spaghetti” is an improvement on the “Gadi Currencies” (currently not shared). You can use it – it’s good enough and you got many screenshots on how to use. EURUSD * USDJPY = EURJPY, so why do you need it? G.

OMG, you are right about EURJPY …. and thanks a lot for “Gadi Currencies” and others …

Edit : Could you please give me a clue on how to get value of each Currency (total 8 currencies) from that 7 major pairs (without cross pair) ? Thanks in advanceTake a look at the example of EURJPY (cross): it is built with EURUSD and USDJPY. If you buy EURUSD and buy USDJPY – you basically SELL the USD in EURUSD and BUY the USD in USDJPY. Since you sell and buy the USD at the same time, it is eliminated – and you are left with EURJPY (EUR bought and JPY sold). The same goes to EURGBP which is built by EURUSD & GBPUSD. Since the USD is on the same side in those cases we just DIVIDE the EURUSD/GBPUSD = EURGBP. Same goes to each and every one of the other 21 crosses. G.

Thanks G. And how can i get the USD or EUR currency only , so i can do : USD = z * USD ?

You need to find the diff movement of each currency pair. (d) is the diff between current and previous price, or other factor. You shouls decide what are the optimized definitions of “current” and “previous” price. USD = (EURUSDd + GBPUSDd + AUDUSDd + NZDUSDd + USDCHFd + USDJPYd + USDCADd) /7 The above result can be multilied by the currency market share, or other factor(s). G.

Thanks a lot G

-

This reply was modified 11 years, 2 months ago by

- AuthorPosts

- You must be logged in to reply to this topic.